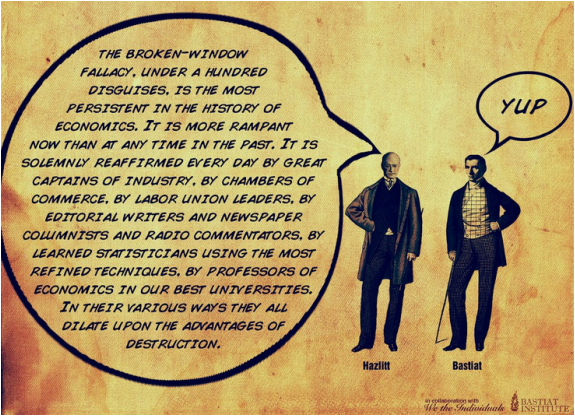

The Broken Window

The other day my neighbor told me he'd lost his job. So, I says to myself “Hey, if I break my other neighbors window, he'll have to replace it. Meaning, he'll have to hire someone to fix it, thus creating economic activity. With the creation of this new economic activity there will be more jobs and my neighbor can get hired and get back to being gainfully employed!”

So, I headed out, rock in hand and smashed my other neighbor's window. Unfortunately, he called the police. He did this even after I explained that I broke his window for a good reason. But, he didn't seem to care. Before you know it, I was arrested and thrown in jail for vandalism, forcing me to post bail, using up what little money I had. This meant I couldn't buy food or gas, so I lost my job and my wife divorced me for being a moron. All of this bad stuff happened because I was trying to help someone. “Damn!” I thought, “could this be karma?” No, it wasn't karma. It was what economists call "The Misallocation of funds.”

This simply means that my attempt to create economic activity and get some gainful employment for my neighbor caused my other neighbor to spend money he didn't really have, on something he didn't really want, leaving him unable to buy things he actually needed like; food, rent, pay his utilities, you know, the basics. This meant that I had created some economic activity; the bail company made out, the police earned their salary, the courts made a few bucks, but my friend still didn't have a job, I no longer had a wife—and, my other neighbor had more problems as the result—thus, “The Misalocation of funds.”

What is the moral of this story? Printing and spending money can give a momentary boost to the economy, few would argue against that. However, when governments compel people to buy what they don’t really want or need by manipulating economic activity (artificially low interest rates or massive money printing schemes) for instance, those businesses that are the prime beneficiaries, tend to thrive only as long as the borrowed money lasts. When it dries up (and it always does) those same businesses collapse like a house of cards.

And that, my friends, is where we are as a nation, and have been for the better part of two decades, living in a house of cards, propped up by an artificial economy, all of which was induced by central banks and bad fiscal policy from our political leaders in Washington. This is true of the Housing boom and bust, as well as the previous recession brought on by Dot. Com. boom and bust. We are living in a debt-based world of bursting bubbles, leaving a trail of financial wreckage in their wake.

Finally, no one is better at determining what you really need, than you are, far better than some distant politician or bureaucrat, that's for certain. It is, after all, your money, that you've earned. It should be your choice where you spend it. If enough people do likewise, businesses will be far more likely to survive and thrive for the simple reason that they provide a good or service that people actually want. That is how a free economy, a free people actually live. Don't let anyone tell you otherwise.

Mark Magula

So, I headed out, rock in hand and smashed my other neighbor's window. Unfortunately, he called the police. He did this even after I explained that I broke his window for a good reason. But, he didn't seem to care. Before you know it, I was arrested and thrown in jail for vandalism, forcing me to post bail, using up what little money I had. This meant I couldn't buy food or gas, so I lost my job and my wife divorced me for being a moron. All of this bad stuff happened because I was trying to help someone. “Damn!” I thought, “could this be karma?” No, it wasn't karma. It was what economists call "The Misallocation of funds.”

This simply means that my attempt to create economic activity and get some gainful employment for my neighbor caused my other neighbor to spend money he didn't really have, on something he didn't really want, leaving him unable to buy things he actually needed like; food, rent, pay his utilities, you know, the basics. This meant that I had created some economic activity; the bail company made out, the police earned their salary, the courts made a few bucks, but my friend still didn't have a job, I no longer had a wife—and, my other neighbor had more problems as the result—thus, “The Misalocation of funds.”

What is the moral of this story? Printing and spending money can give a momentary boost to the economy, few would argue against that. However, when governments compel people to buy what they don’t really want or need by manipulating economic activity (artificially low interest rates or massive money printing schemes) for instance, those businesses that are the prime beneficiaries, tend to thrive only as long as the borrowed money lasts. When it dries up (and it always does) those same businesses collapse like a house of cards.

And that, my friends, is where we are as a nation, and have been for the better part of two decades, living in a house of cards, propped up by an artificial economy, all of which was induced by central banks and bad fiscal policy from our political leaders in Washington. This is true of the Housing boom and bust, as well as the previous recession brought on by Dot. Com. boom and bust. We are living in a debt-based world of bursting bubbles, leaving a trail of financial wreckage in their wake.

Finally, no one is better at determining what you really need, than you are, far better than some distant politician or bureaucrat, that's for certain. It is, after all, your money, that you've earned. It should be your choice where you spend it. If enough people do likewise, businesses will be far more likely to survive and thrive for the simple reason that they provide a good or service that people actually want. That is how a free economy, a free people actually live. Don't let anyone tell you otherwise.

Mark Magula